Why Use Multiple Payment Options to Boost Sales

TL;DR:

- Offering multiple payment options significantly reduces cart abandonment and increases checkout completion rates.

- Understanding regional and demographic preferences ensures better customer trust, loyalty, and global market access.

- Using payment orchestration platforms simplifies management and maximizes conversion through intelligent routing and unified settlement.

Offering multiple payment options is the single most direct lever a business can pull to increase checkout completion rates and reduce lost revenue. When customers reach the payment screen and cannot find their preferred method, they leave. That friction is not a minor inconvenience. It is a conversion killer with measurable consequences. Platforms like Apple Pay, Klarna, and PayPal have normalized payment flexibility as a baseline expectation, not a premium feature. Understanding why multiple payment options matter, and how to deploy them strategically, separates businesses that grow from those that stall at the final step.

Why use multiple payment options to reduce cart abandonment

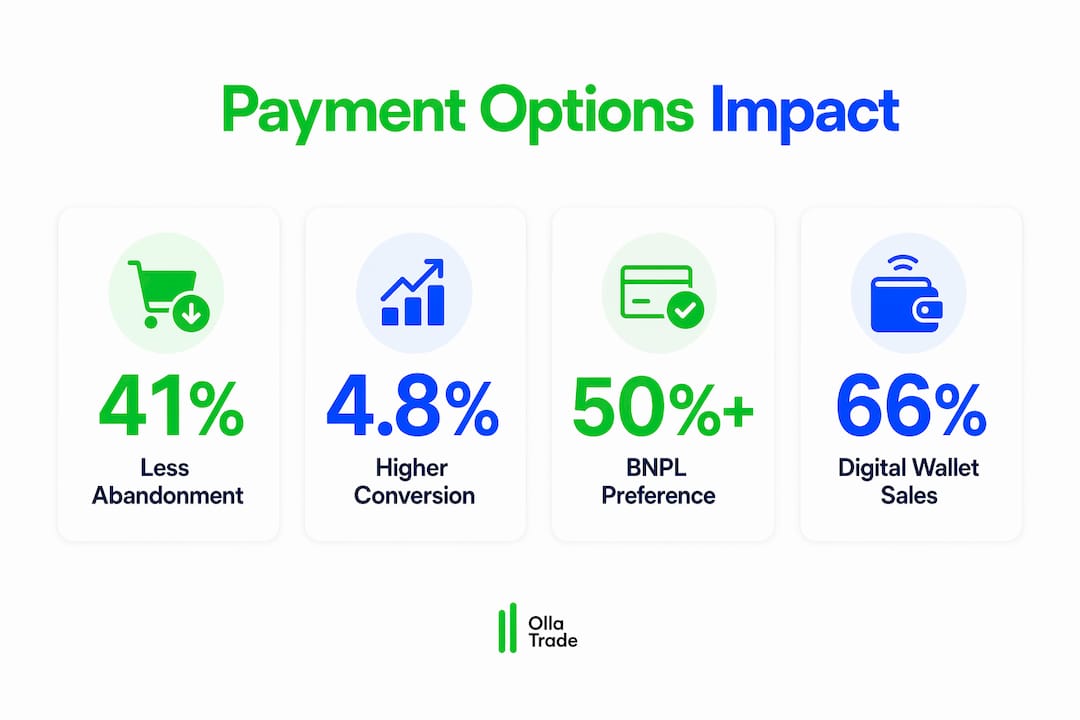

The data on payment variety and cart abandonment is not subtle. Stores offering multiple payment options saw a 41% decrease in cart abandonment compared to single-method checkouts. That number represents real customers who had already decided to buy, then stopped because the checkout could not meet them where they were.

The conversion gap is equally striking. Stores with six or more payment methods averaged a 4.8% conversion rate versus 2.9% for single-option checkouts. For a business processing 10,000 monthly visitors, that difference translates directly into hundreds of additional completed transactions without spending a dollar on additional traffic.

The root cause is straightforward. Customers have developed strong payment habits tied to trust, convenience, and financial management. A shopper who relies on Klarna for budget control, or who uses Apple Pay for speed, will not switch to a credit card entry form just because that is all you offer. They will simply find a competitor who accommodates them.

Common reasons customers abandon at the payment stage include:

- Their preferred digital wallet is not supported

- Buy Now, Pay Later options are absent for higher-ticket purchases

- The checkout requires too many manual card entry steps

- Local or regional payment methods are unavailable for international buyers

Pro Tip: Display your available payment method logos prominently at the top of the checkout page, not just at the point of entry. Customers who see their preferred method early are far less likely to hesitate later in the flow.

Which payment methods matter most by demographic and region

Payment preference is not universal. It is shaped by age, geography, and purchasing behavior. Treating all customers as if they share the same payment habits is one of the most common and costly mistakes in checkout design.

BNPL options are preferred by over 50% of Gen Z and millennials, and they directly increase average order values for high-ticket items. This is not simply a generational quirk. BNPL shifts the psychological framing of a purchase from “can I afford this now” to “can I manage this over time,” which unlocks spending that would otherwise not happen. For Gen X buyers, traditional credit and debit cards remain dominant, and removing friction from card entry still matters enormously for that demographic.

Regional variation adds another layer of complexity. Enabling local payment methods increases checkout conversion by 51% for internationally expanding businesses. In Germany, Sofort and SEPA bank transfers are standard expectations. In the Netherlands, iDEAL handles the majority of online transactions. In Brazil, Pix and Boleto Bancário are not alternatives. They are the primary methods. Ignoring these preferences means writing off entire markets.

The macro trend reinforces the urgency. Non-card payments, led by digital wallets, accounted for 66% of global online sales by March 2026. Pay-by-bank transfers grew by 40% in 2024 and made up 25% of digital retail payments by 2025. These are not niche behaviors. They represent the mainstream direction of global commerce.

| Payment Method | Primary Demographic | Key Regions |

|---|---|---|

| Digital wallets (Apple Pay, Google Pay) | Millennials, Gen Z | North America, Europe, Asia-Pacific |

| BNPL (Klarna, Afterpay) | Gen Z, Millennials | US, UK, Australia, Nordics |

| Credit/Debit cards | Gen X, Baby Boomers | Global, especially North America |

| Local bank transfers (iDEAL, Pix, Sofort) | All ages | Netherlands, Brazil, Germany |

| Cryptocurrency | Tech-savvy, younger traders | Global, growing in emerging markets |

Pro Tip: Before expanding into a new market, survey your existing customer base in that region or analyze your payment failure data. The methods causing the most drop-offs tell you exactly where to invest first.

How to implement multiple payment gateways without operational chaos

Adding payment options sounds straightforward until you are managing five separate gateway contracts, reconciling funds across multiple accounts, and troubleshooting conflicting fraud rules. The operational complexity is real, and it is the primary reason many businesses delay diversifying their payment stack.

Payment orchestration platforms solve this problem directly. Rather than connecting each gateway independently, orchestration layers sit above all payment providers and manage routing, fallback logic, and reporting from a single interface. Businesses using payment orchestration platforms see 23% higher conversion rates than those managing multiple gateways separately. The performance gain comes from dynamic routing, which automatically directs transactions to the gateway most likely to approve them based on card type, geography, and real-time success rates.

Key capabilities that payment orchestration platforms provide include:

- Dynamic routing: Sends each transaction to the optimal gateway in real time

- A/B testing: Lets you test payment method presentation and ordering without developer involvement

- Unified settlement: Consolidates receipts from multiple payment methods into a single business account, eliminating the need to manage multiple bank accounts

- Fraud prevention integration: Applies consistent AI-powered fraud rules across all channels, which reduces declined legitimate transactions by 29%

Providers like Adyen, Gr4vy, and Stripe offer orchestration capabilities at different price points and complexity levels. The right choice depends on transaction volume, geographic reach, and internal technical resources.

Pro Tip: High-converting stores focus on a curated 4 to 6 payment methods aligned with their specific customer profile. More options beyond that threshold can overwhelm users and slow checkout completion. Start with your top-performing methods and expand based on data.

How payment flexibility builds customer trust and loyalty

Payment experience and brand perception are inseparable in the customer’s mind. Consumers rarely separate payment performance from brand trust, and a single failed or frustrating transaction can undo months of positive brand-building. This is not a soft concern. It has direct revenue implications through churn, refund requests, and lost repeat business.

The positive side of this equation is equally powerful. When a checkout experience feels effortless, it reinforces the customer’s confidence in the brand as a whole. Features like biometric authentication through Apple Pay or Google Pay reduce checkout time to seconds. Accelerated checkout options that remember payment details eliminate the friction of re-entry on repeat visits. These are not luxury features. They are now baseline expectations for customers who shop regularly online.

Displaying payment options prominently increases completion rates by 31%, and dynamically ordering payment methods based on user behavior adds an 18% uplift on top of that. The implication is clear: the visual presentation of payment options is itself a conversion tool, not just a functional requirement.

“Payment flexibility is now a front-line brand differentiator impacting loyalty and repeat business.” — Gr4vy

The businesses that treat payment strategy as a backend operational task consistently underperform those that treat it as a customer experience priority. Ignoring diverse payment preferences turns customers away at the exact moment they are most ready to buy. That is the worst possible place to lose them.

Key takeaways

Multiple payment options directly increase conversion rates, reduce abandonment, and build customer loyalty by meeting buyers at their preferred point of transaction.

| Point | Details |

|---|---|

| Abandonment drops with variety | Stores with diverse payment methods see 41% less cart abandonment than single-option checkouts. |

| Demographics drive method preference | BNPL suits Gen Z and millennials; cards remain dominant for Gen X; local methods are critical internationally. |

| Orchestration reduces complexity | Payment orchestration platforms deliver 23% higher conversions and unify settlement into one account. |

| Visibility increases completion | Prominently displaying payment options at checkout raises completion rates by 31%. |

| Payments are a brand signal | Poor payment experiences damage trust and drive churn, making flexibility a front-line business priority. |

The case for treating payments as strategy, not infrastructure

Most businesses I have observed treat payment setup as a one-time technical task. You pick a gateway, integrate it, and move on. That mindset is the source of most payment-related revenue leakage I have seen, and it is surprisingly common even among otherwise sophisticated operators.

The businesses that consistently outperform on conversion treat payment strategy the way they treat pricing or product selection: as something that requires ongoing attention, testing, and localization. The role of payment options in trading efficiency is a perfect example of this principle applied to financial platforms, where deposit and withdrawal friction directly affects whether a user activates and stays active.

My honest view is that the “more is better” instinct is wrong. Stacking fifteen payment methods onto a checkout page does not signal flexibility. It signals confusion. The discipline is in selecting the four to six methods that your specific customer base actually uses, then presenting them in a way that feels personal and frictionless. That requires payment data analysis, not guesswork.

Localization is the most underutilized lever I see. A business expanding into Southeast Asia that only offers Visa and Mastercard is leaving a significant portion of the market unreachable. Supporting AED-based regional payment preferences or local bank transfer methods in target markets is not a nice-to-have. It is the price of entry. The 51% conversion lift from local payment methods is not a marginal improvement. It is a structural advantage.

The final point I would make is about monitoring. Payment performance data, approval rates by method, failure reasons by geography, and abandonment points by device, is some of the richest behavioral data a business generates. Most businesses collect it and ignore it. The ones that review it monthly and adjust their payment stack accordingly are the ones that compound their conversion gains over time.

— FX

Start trading with flexible payment options on Ollatrade

Ollatrade is built for traders who expect their platform to work as hard as they do. Depositing and withdrawing funds should never be the reason a trade is delayed or a position is missed. Ollatrade supports a broad range of payment methods for deposits and withdrawals, so you can move capital on your terms, not the platform’s. Whether you are accessing Forex markets or trading CFDs on metals, indices, and cryptocurrencies, the payment experience is designed to be fast, secure, and flexible. Explore Ollatrade today and set up your account with the payment method that works best for you.

FAQ

Why do multiple payment options reduce cart abandonment?

When customers reach checkout and cannot find their preferred payment method, 20% abandon the purchase immediately. Offering diverse options removes that friction and keeps buyers in the flow.

What is the best number of payment methods to offer?

High-converting stores focus on four to six core payment methods aligned with their customer profile. Offering more than that can overwhelm users and slow checkout completion without meaningfully increasing conversions.

How does BNPL affect average order value?

Buy Now, Pay Later options like Klarna and Afterpay increase average order values for high-ticket items by shifting the buyer’s focus from total cost to manageable installments. BNPL is preferred by over 50% of Gen Z and millennial shoppers.

What is a payment orchestration platform?

A payment orchestration platform sits above multiple payment gateways and manages routing, fraud detection, and settlement from a single interface. Businesses using orchestration see 23% higher conversion rates than those managing gateways separately.

How do local payment methods affect international sales?

Enabling local payment methods increases checkout conversion by 51% for internationally expanding businesses. Methods like iDEAL in the Netherlands, Pix in Brazil, and Sofort in Germany are not alternatives for local buyers. They are the primary payment channels.

Recommended

Articles are for informational and educational purposes only and do not constitute investment advice. Trading CFDs carries significant risk of loss. Past performance is not a reliable indicator of future results. Olla Trade Ltd. is an Anguilla registered entity.